Credit scores normally vary in between 300 to 850 on the FICO scale, from poor to excellent, computed by three major credit bureaus (TransUnion, Experian and Equifax). Keeping your credit complimentary and clear of timeshare value financial obligation and taking the steps to enhance your credit rating can qualify you for the best mortgage rates, fixed or adjustable.

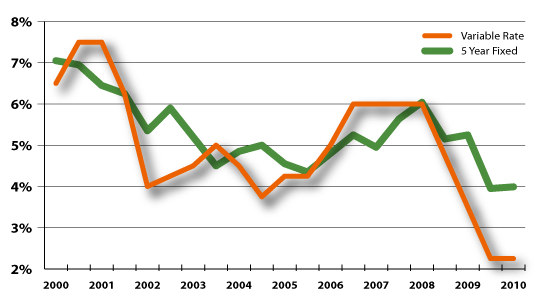

They both share resemblances in that being successfully prequalified and preapproved gets your foot in the door of that new home, but there are some differences. Supplying some basic financial details to a property representative as you look around for a house, like your credit report, current earnings, any debt you may have, and the quantity of savings you might have can prequalify you for a loan-- essentially a method of allocating you in advance for a low-rate loan prior to you've gotten it. When you're shopping for a loan, remember: Lower preliminary rate which might be locked for an introductory period or set timeframe Rate changes on pre-determined dates (e. g., annual, 3-, 5-, 7-year terms) Great option if rates of interest are high and/or if you just plan to remain in the home for a short time Interest rate remains the exact same over the life of the loan Predictable regular monthly paymentseven if rates of interest increase, your payment doesn't alter Great choice if rates of interest are low and/or you prepare to stay in the home for a long time Sometimes these terms are used interchangeably, however they're actually extremely various: This includes providing your lender with some fundamental informationwhat earnings you make, what you owe, what assets you have, and so on.

When you get pre-qualified, the lender does not examine your credit report or make any decision if you can certify for a mortgagethey'll just provide the home mortgage quantity for which you might qualify. Pre-qualifying can help you have an idea of your financing amount (and the process is generally quick and totally free), however you won't know if you actually get approved for a mortgage up until you get pre-approved. how many mortgages in the us.

You'll typically need to pay an application fee, and the loan provider pulls and evaluates your credit. A pre-approval takes longer than a pre-qualification as it's a more comprehensive evaluation of your finances and credit merit. Pre-approval is a bigger step however a much better commitment from the loan provider. If you certify for a mortgage, the loan provider will have the ability to supply: the quantity of funding; potential rates of interest (you might even have the ability to lock-in the rate); and you'll be able to see a quote of your month-to-month payment (prior to taxes and insurance coverage due to the fact that you have not found a property yet).

Likewise, you're letting sellers know you're a serious and certified buyer. Typically, if there's competition for a house, purchasers who have their funding in location are chosen since it shows the seller you can manage the home and are all set to acquire. We'll likewise go through the pre-approval process a bit more in the next area.

The rates of interest is what the lending institution charges you to borrow cash. The APR consists of the rates of interest as well as other fees that will be consisted of over the life of the loan (closing costs, fees, etc) and reveals your total yearly expense of borrowing. As an outcome, the APR is greater than the basic interest of the home loan.

The Only Guide for Which Of The Following Statements Is Not True About Mortgages?

In addition, all loan providers, by federal law, need to follow the exact same guidelines when determining the APR to make sure precision and consistency. One point is equivalent to one percent of the total principal quantity of your mortgage. For example, if your home mortgage amount is going to be $125,000, then one point would equal $1,250 (or 1% of the amount financed).

Lenders often charge indicate cover loan closing costsand the points are typically collected at the loan closing and might be paid by the borrower (homebuyer) or home seller, or may be divided between the purchaser and seller. This may depend upon your regional and state policies along with requirements by your loan provider.

Be sure to ask if your home loan consists of a pre-payment charge. A pre-payment penalty implies you can be charged a fee if you pay off your home mortgage early (i. e., pay off the loan before the loan term expires). When you get a mortgage, your lending institution will likely utilize a standard type called a Uniform Residential Mortgage Application, Kind Number 1003.

It is essential to offer accurate information on this type. The type includes your individual information, the purpose of the loan, your earnings and assets and other info needed throughout the certification procedure - how do down payments work on mortgages. After you offer the lender six pieces of information your name, your income, your social security number to get a credit report, the property address, a price quote of the worth of the residential or commercial property, and the size of the loan you desire your lender should offer or send you a Loan Quote within 3 days.

e., loan type, rate of interest, estimated regular monthly mortgage payments) you went over wyndham timeshare presentation with your lending institution. Thoroughly examine the price quote to be sure the terms fulfill your expectations. If colorado timeshare anything appears different, ask your lender to explain why and to make any needed corrections. Lenders are required to offer you with a written disclosure of all closing conditions 3 service days prior to your arranged closing date.

e, closing costs, loan amount, rate of interest, monthly home loan payment, approximated taxes and insurance beyond escrow). If there are substantial modifications, another three-day disclosure period might be required.

Why Do Banks Sell Mortgages To Other Banks - The Facts

Unless you can buy your home totally in money, discovering the ideal home is only half the battle. The other half is selecting the very best type of home loan. You'll likely be repaying your mortgage over a long duration of time, so it's essential to discover a loan that satisfies your requirements and budget plan.

The two primary parts of a home mortgage are primary, which is the loan amount, and the interest charged on that principal. The U.S. government does not operate as a mortgage lending institution, but it does ensure particular kinds of mortgage. The 6 main kinds of home mortgages are standard, conforming, non-conforming, Federal Housing Administration-insured, U.S.

Department of Agriculture-insured. There are two components to your home loan paymentprincipal and interest. Principal refers to the loan quantity. Interest is an extra quantity (computed as a portion of the principal) that lending institutions charge you for the benefit of borrowing money that you can repay over time. During your mortgage term, you pay in monthly installations based on an amortization schedule set by your lender.

APR consists of the rates of interest and other loan costs. Not all home loan items are produced equivalent. Some have more rigid guidelines than others. Some loan providers might require a 20% deposit, while others require as low as 3% of the home's purchase rate. To receive some types of loans, you require pristine credit.